Market Scenario

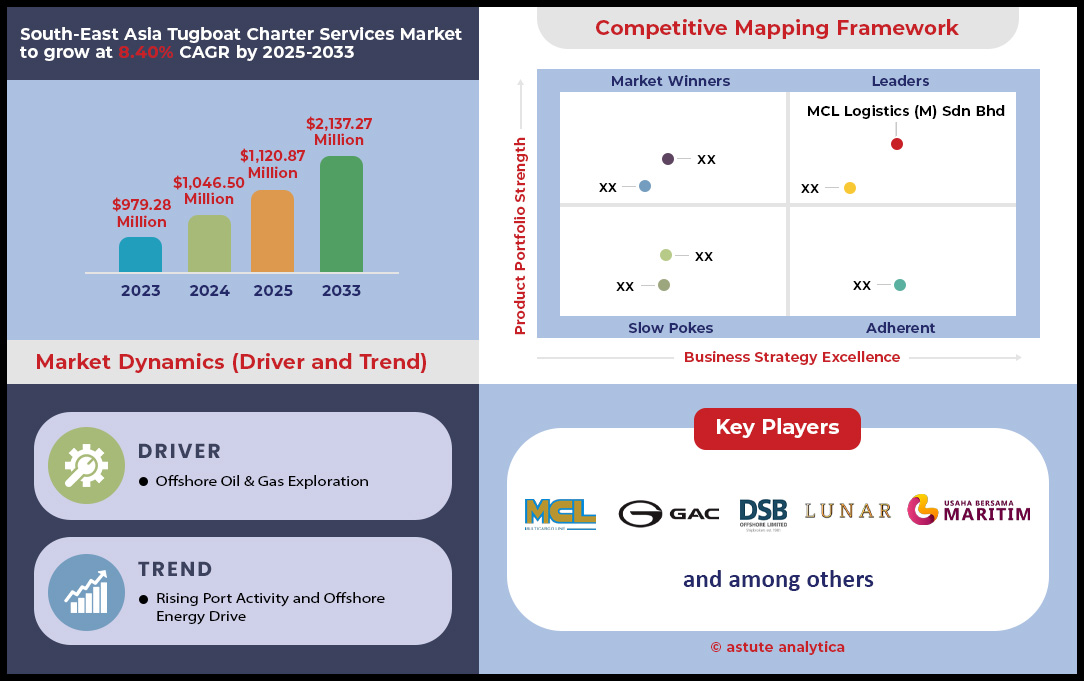

South-East Asia tugboat charter services market was valued at US$ 1,046.50 million in 2024 and is projected to hit the market valuation of US$ 2,137.27 million by 2033 at a CAGR of 8.40% during the forecast period 2025–2033.

Key Findings in South Asia Tugboat Charter Services Market

- Terminal tugs with over 21.08% market share are currently witnessing the highest demand in the South East Asia tugboat charter services.

- It has been found that over 22.45% of all demand for tugboat charter services in the regions is mainly witnessed for vessels having 5000-8000 HP power.

- When it comes to application, tug boat charter services with over 26.07% market share are primarily used for harbor & deep-sea carrier.

- Today, third party operators with over 54.76% emerged as the largest providers in the South East Asia market.

- Singapore is the largest market with over 34% market share

- South-East Asia tugboat charter services market is poised to reach US$ 2,137.27 million by 2033.

An exceptional demand landscape is unfolding across the South-East Asia tugboat charter services market, unlocking unprecedented opportunities. The market is fueled by two powerful parallel engines of growth. First, port activity is creating a surge in harbor towage demand, with Port Klang’s record 14.64 million TEUs in 2024 and its 15 million TEU target for 2025 signaling thousands of additional vessel movements. Second, a revitalized energy sector is generating a voracious appetite for offshore support. Petronas plans to drill 99 wells and operate 28 rigs in 2024, coupled with a forecast of 39.2 active jack-up units across the region in 2025, guaranteeing a high tempo for AHTS charters.

Beyond sheer volume, the nature of demand is becoming more sophisticated and lucrative. The development of major LNG infrastructure in the tugboat charter services market, such as the 3.3 billion facility in Batangas, is creating a new premium market for specialized, high-power tugs. Operators are already delivering, with PSA Marine’s new builds featuring a 64.6-tonne bollard pull. This demand for higher specifications allows leading players to secure high-value, long-term work. A prime example is the two-year, RM41 million (USD 9.16 million) contract awarded for project support, underpinning work on massive undertakings like the fabrication of four new Central Processing Platforms and the installation of 1,130 km of pipelines.

A deeply embedded pipeline of government-backed and commercially sanctioned projects provides remarkable forward visibility for investors and operators. Indonesia’s SKK Migas is driving an immense wave of activity, targeting 133 upstream projects to come online by 2029, with 15 of those slated for 2024. These are not distant goals; tangible projects like the Mako gas field are scheduled to add 120 MMSCFD of production in Q4 2025. This concrete, multi-year project roadmap solidifies a golden era of opportunity and growth for the South-East Asia tugboat charter services market.

To Get more Insights, Request A Free Sample

Future-Proofing Fleets Defines Next Wave of Market Opportunity in Southeast Asia Tugboat Charter Services Market

- Pioneering Green Corridors and Alternative Fuels: A powerful trend towards decarbonization is reshaping vessel requirements. Singapore is a key driver, establishing green and digital shipping corridors with Australia and China's Shandong province in 2024 to pilot sustainable practices and the use of low-carbon fuels. The initiative encourages the adoption of alternative fuels, with plans for bio-LNG bunkering pilots scheduled for 2024 and 2025. Reflecting the move towards fuel readiness, major regional shipping lines like Pacific International Lines have already ordered 8 new ammonia-ready container ships, creating future demand for tugs that can support these next-generation vessels.

- Embracing Digitalization and Remote Operations: Major operators in the South-East Asia tugboat charter services market are leveraging digitalization to enhance safety and efficiency, a trend creating demand for technologically advanced tugs. PSA Marine is expanding its Fleet D2K Centre capabilities in 2024, enabling real-time remote monitoring of vessel machinery and fuel consumption on more of its tugs. The company's IntelliTug project has already validated the use of remote joystick control for harbor tugs in the busy Port of Singapore, setting a new benchmark for operational capability. A push towards smarter operations includes using AI for speed optimization and exploring fully remote supervision, indicating a future where digitally integrated tugs are essential.

- Capturing the Emerging Offshore Wind Market: The nascent offshore wind sector is transitioning to a major source of long-term demand for a variety of support vessels. Vietnam's ambitious Power Development Plan 8 (PDP8) now targets up to 17GW of offshore wind by 2035, a monumental goal requiring extensive marine support. To meet the build-out across Asia, demand for specialized vessels is projected to outpace supply significantly, with one estimate showing a need for over 145 additional commissioning service operation vessels (CSOVs) by 2030, a fleet that requires tug support for port operations and logistics. Owners of anchor-handling tugs are particularly well-positioned, as the greater number of floating wind installations planned will drive a significant call on their specialized capabilities.

Raw Material Transport and Barge Logistics Fuel Essential Market Demand

A foundational demand driver for the South-East Asia tugboat charter services market is the immense volume of raw material transport. Regional economies rely heavily on tug and barge combinations for moving essential commodities. Indonesia’s coal sector is a prime example. The Ministry of Energy and Mineral Resources set a massive coal production target of 710 million tonnes for 2024. A significant portion of this volume is transported via river systems, a logistical feat that prompted Indonesian companies to order at least 200 new tug and barge sets in the first half of 2024 alone. Similarly, the Philippines aims to ship over 35 million wet metric tons of nickel ore in 2024, a trade conducted almost exclusively with tug and barge flotillas.

The demand extends beyond mining in the tugboat charter services market. In Vietnam, the Vissai Group plans to transport 5 million tonnes of cement and clinker via waterways in 2024, utilizing its dedicated fleet of over 100 tugs and barges. Infrastructure development further fuels this segment. More than 3,000 sand-carrying barge voyages are projected between Indonesia and Singapore for construction projects in 2024. Meanwhile, a single major data center campus in Johor, Malaysia, will require an estimated 1,500 barge voyages for materials through 2025. This demand is also supported by infrastructure upgrades, such as the Cikarang-Bekasi Laut canal enhancement, which will accommodate larger 4,000-tonne barges by 2025, ensuring the continued relevance of this market segment.

Naval Fleet Expansion Creates a Stable Demand for Specialized Tug Support

A significant and stable source of demand for the South-East Asia tugboat charter services market originates from regional naval fleet modernization and security operations. Governments are making substantial investments in maritime capabilities, creating a consistent need for tug support. The Philippine Navy, for instance, is expecting the delivery of 2 new corvettes and 4 new fast attack craft in 2025. In parallel, Indonesia's PT PAL shipyard is scheduled to begin delivering 2 new "Merah Putih" frigates to its navy in 2025. Each of these new, high-value naval assets will require professional tug services for all berthing, unberthing, and port maneuvers throughout their operational lives.

This demand is bolstered by frequent international cooperation and strategic port usage. Singapore’s Changi Naval Base is a key hub, having hosted more than 80 foreign naval vessel port calls in 2024. Large-scale military exercises, such as SEACAT 2024 which involved vessels from 24 nations, create periods of intense, concentrated demand for local tug operators. The US Navy alone has scheduled at least 12 logistics and resupply operations at Singaporean ports for its Littoral Combat Ship fleet in 2024. Furthermore, the Malaysian Navy conducted over 30 multilateral exercises in 2024. Even end-of-life naval operations, such as the sinking of 5 decommissioned vessels to create artificial reefs in 2025, require specialized tug charters, providing a steady, non-commercial revenue stream for the market.

Segmental Analysis

Terminal Tugs Command Vital Role in Bustling Regional Ports

The pronounced dominance of terminal tugs within the South-East Asia tugboat charter services market is a direct consequence of the region's burgeoning port activity and infrastructure growth. In 2024, Singapore's port saw vessel arrivals reach a record 3.11 billion gross tons and handled an unprecedented 41.12 million TEUs, underscoring the sheer volume of ships requiring assistance. This intense traffic is managed by a growing fleet of terminal tugs designed for the precise maneuvering essential for berthing and unberthing the world's largest ships. The 16% increase in the average vessel call size since 2019 further solidifies the need for these specialized assets. The market's health is reflected in the high performance of its hubs, with 13 of the top 20 most efficient ports globally situated in the broader Asian region.

Terminal tugs are indispensable for maintaining the operational fluidity of the world's most critical transshipment hubs. Their importance is magnified by the fact that total cargo throughput in Singapore alone climbed to 622.67 million tonnes in 2024. The continuous investment in port expansion, such as at Malaysia's Port Klang which handled 14.64 million TEUs in 2024, ensures that demand for these workhorses remains robust. The entire ecosystem of the South-East Asia tugboat charter services market relies on the efficiency of terminal operations to prevent congestion and sustain the flow of global trade.

- In the first four months of 2024, monthly average container vessel arrivals in Singapore reached 72.4 million gross tonnage.

- Leading operator PSA handled a milestone 100.2 million TEUs across its global network in 2024.

- Over 182,000 individual vessel calls were analyzed for the 2023 global port performance report, highlighting the scale of terminal operations.

High-Powered Tugs Propel Deepwater and Offshore Ambitions

The escalating demand for tugboats in the 5000-8000 HP range is intrinsically linked to two powerful trends shaping the South-East Asia tugboat charter services market: the growth of ultra-large vessels and the aggressive expansion into deepwater energy projects. Handling modern mega-ships requires immense power and precision, which this class of tug delivers. Simultaneously, the region is unlocking vast offshore resources, with a projected $100 billion in offshore gas investments expected by 2028. This exploration and production boom creates a substantial need for high-horsepower tugs for anchor handling, rig positioning, and long-distance towing of critical infrastructure.

The scale of these new energy ventures is staggering. Recent discoveries like the Layaran-1 (6 TCF) and Geng-North 1 (5 TCF) gas fields in Indonesia, alongside the development of the 18 TCF Abadi field, necessitate a powerful support fleet. Furthermore, with over 50 FPSO projects on the global horizon by 2029 and a single S$11 billion contract for two such vessels in Singapore, the requirement for robust tugs is clear. The burgeoning offshore wind sector, with 122 GW of capacity expected in APAC by 2030, adds another layer of demand, securing a dominant role for high-HP tugs in the evolving South-East Asia tugboat charter services market.

- Capital commitments for new offshore projects in Southeast Asia hit approximately $30 billion for the 2024-2025 period.

- Each of the two new FPSOs being built in Singapore will have a production capacity of 225,000 barrels of oil per day.

- Vietnam and Singapore are collaborating on a significant offshore wind farm project scheduled to start in 2030.

Harbor and Deep-Sea Applications Generate Unmatched Market Revenue

The harbor and deep-sea application segment commands the largest revenue share in the South-East Asia tugboat charter services market due to a powerful combination of high-volume port activities and high-value offshore projects. Harbor services, driven by the constant flow of vessels, create a steady and predictable revenue stream. In Singapore, a single operator like PSA Marine performs over 100,000 tug moves annually, while total bunker sales of 54.92 million tonnes in 2024 signify a massive number of port calls requiring tug assistance. The region’s status as the world’s maritime crossroads, processing a significant portion of the 937 million TEUs moved globally in 2024, ensures relentless demand for in-port towage.

This foundational revenue from harbor towage is powerfully supplemented by lucrative deep-sea charters. These projects, supporting the oil, gas, and renewables sectors, involve long-term contracts at premium rates. The planned decommissioning of 60 offshore platforms in Brunei and the 19 new exploration discoveries in Malaysia in 2023 highlight the long-term nature of this demand. As the tugboat charter services market moves further offshore, the complexity and value of these services increase, cementing the dominance of this application segment. The forecast demand of over 600 vessel years for OSVs in Asia by 2026 confirms the sector's robust future.

- The total tonnage of ships flying the Singapore flag surpassed 100 million GT for the first time in 2024.

- Global port efficiency in 2023 was assessed based on 238.2 million individual container movements.

- By 2030, the Asia-Pacific's offshore wind industry will require an estimated 35-40 specialized Service Operations Vessels.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Third-Party Operators Emerge as Undisputed Market Leaders

Specialized third-party firms have solidified their position as the dominant force in the South-East Asia tugboat charter services market, driven by industry-wide trends of outsourcing and fleet modernization. Port authorities and global shipping lines increasingly focus on their core business, entrusting towage operations to independent companies that offer greater efficiency, flexibility, and cost savings. These operators are aggressive in renewing their fleets, as evidenced by the nearly 150 new tugs delivered from regional shipyards in 2024 and a global order book for 392 new tugs. This continuous investment ensures they have the modern, powerful, and diverse vessels required for any task.

The expansion of these independent players is rapid, with over 30 maritime companies establishing or growing their Singapore operations in 2024. The operational scale is significant; PSA, for instance, handled 59.2 million TEUs in 2024 at its terminals outside its Singapore headquarters. Furthermore, supportive regulations in key markets, such as Indonesia's cabotage laws that favor domestic operators, create a fertile ground for these third-party companies to thrive. Their specialized focus and ability to achieve economies of scale make them the undisputed leaders, shaping the competitive landscape of the South-East Asia tugboat charter services market.

- In the final quarter of 2024, Vietnamese shipyards built 17% of all tugs delivered worldwide.

- Malaysian shipyards were also significant contributors, producing 8% of the global tug deliveries in Q4 2024.

- Indonesia's Law No. 17 of 2008 mandates the use of domestically flagged vessels for internal shipping routes.

To Understand More About this Research: Request A Free Sample

Country Analysis

Singapore's Leadership Forged Through Advanced Capabilities and Intense Maritime Activity

Singapore's dominant position with over 34% market share in the South-East Asia tugboat charter services market is built on unmatched operational intensity and strategic investments. The nation's maritime pulse is relentless, with vessel arrival tonnage hitting an incredible 807 million gross tons in just the first quarter of 2024. During the same period, container throughput reached 9.9 million TEUs, driving constant demand for harbor towage. The port's role as a global bunkering hub is a significant factor, with bunker sales volume reaching 13.8 million tonnes in Q1 2024, an activity requiring extensive barge and tug support. This core activity is supplemented by a thriving ship repair sector; major yard Seatrium secured 2 new FPSO integration contracts in 2024, necessitating numerous complex tug movements.

The nation's focus extends to specialized and future-focused segments. The SLNG terminal conducted its 100th small-scale LNG reload operation in mid-2024, highlighting its growing niche importance in the tugboat charter services market. Jurong Port targets handling over 15 million tons of bulk cargo in 2024. To support growing barge traffic, the new Tuas Lighter Terminal became operational in 2024 with 17 lighter berths. Looking ahead, Singapore is ordering advanced assets, with PSA Marine expecting delivery of 2 new electric tugs in 2025, one having a 70-tonne bollard pull. The ammonia bunkering pilot for 2025 will also require at least 2 dedicated support tugs, cementing Singapore’s role as a leader in maritime innovation.

Malaysia's Ascendancy Powered by Energy Sector and Strategic Port Growth

Malaysia's strong market position in the tugboat charter services market is propelled by a robust energy sector and ambitious port expansion plans. The Bintulu Port LNG terminal alone is scheduled to handle over 700 vessel calls in 2024. Offshore, Petronas' Kasawari gas project's final commissioning in 2024 requires at least 4 dedicated support vessels. This activity has led to major contract wins, with ICON Offshore securing charters for 5 AHTS vessels in Malaysian waters in 2024. Fabrication yards are also booming; Malaysia Marine and Heavy Engineering secured a major offshore substation contract in 2024, involving 3 major sea transport operations requiring powerful tugs.

Major infrastructure investments are set to dramatically increase future tug demand in the tugboat charter services market. The Port of Tanjung Pelepas is investing RM3 billion to add 3 new berths by 2025. This complements Port Klang Authority’s target of handling 220 million freight weight tonnes of cargo in 2024. Further north, the Sapangar Bay Container Port expansion aims for a capacity of 1.2 million TEUs by 2025. Even naval modernization contributes, with the Malaysian Maritime Enforcement Agency taking delivery of 2 new offshore patrol vessels in 2025. The country also plans to decommission at least 3 offshore platforms in 2025, an operation demanding multiple high-bollard pull tugs.

Strategic Investments and Consolidation Signal a New Era of Market Dominance in South-East Asia Tugboat Charter Services Market

- Bumi Armada Secures Major FPSO Financing: Malaysia's Bumi Armada announced in February 2024 that it had secured a syndicated sustainability-linked financing facility of $384 million. While for a Floating Production Storage and Offloading (FPSO) unit, this funding underpins a major offshore project that requires extensive long-term tug and support vessel services.

- AG&P Makes $3.3 Billion Investment in Philippines LNG: In a joint venture, AG&P subsidiary Linseed Field and two other Philippine energy companies announced a $3.3 billion investment in a major integrated LNG facility in Batangas. The investment covers a new power plant and expansion of LNG terminal services, directly fueling demand for specialized tug support.

- ICON Offshore Secures Major Long-Term Contracts Worth RM196.3M: In May 2024, Malaysia's ICON Offshore secured long-term charter contracts for five of its anchor handling tug supply (AHTS) vessels. The contracts, valued at approximately $41.6 million (RM196.3 million), demonstrate significant investment by oil majors in securing long-term vessel capacity in the tugboat charter services market.

- Perdana Petroleum Secures RM65.5 Million in Contracts: Malaysian OSV operator Perdana Petroleum announced in August 2024 that it had won contracts valued at approximately $13.9 million (RM65.5 million) for the charter of three anchor handling tug and supply vessels. The awards reflect continued strong investment in the Malaysian offshore sector.

- Marco Polo Marine's Strategic Investment in Taiwan Wind Market: While focused on Taiwan, Singapore's Marco Polo Marine's significant investment in a new Commissioning Service Operation Vessel (CSOV), which began construction in early 2024, signals a broader regional strategy. The investment positions the company to serve the burgeoning Southeast Asian offshore wind market as it develops.

- Keppel Acquires FPSO Operator to Boost Recurring Income: Keppel Corporation of Singapore completed its acquisition of FPSO operator Aibel in early 2024. This strategic investment aims to bolster recurring income from energy infrastructure, underpinning the long-term offshore projects that create sustained demand for marine support services.

- Vard Secures Funding for Major Vessel Construction: Vard, a major shipbuilder with a significant yard in Vung Tau, Vietnam, secured various contracts in 2024 for advanced offshore and specialized vessels. The funding for these construction projects, including CSOVs, directly translates into future fleet capacity for the region's energy sector.

- EA Technique Secures RM41 Million Contract Extension: In a significant development for the Malaysian tugboat charter services market, EA Technique announced in November 2024 a two-year contract extension with Petronas for tugboat services valued at approximately $9.16 million (RM41 million), reflecting continued investment in established local operators.

- Tanjung Pelepas Port Commits RM3 Billion for Expansion: The Port of Tanjung Pelepas in Malaysia announced a major investment of RM3 billion ($636 million) for a multi-year expansion. The investment includes the construction of three new berths, a capital outlay that will directly drive demand for an increased number of harbor tugs upon completion.

Top Companies in the South-East Asia Tugboat Charter Services Market

- MCL Logistics (M) Sdn Bhd

- Lunar Shipping Malaysia Sdn Bhd

- DSB Offshore

- KNK Group

- Seaspan ULC

- Swire Pacific Limited

- GAC

- Haivan Ship

- Thoresen-Vinama

- PT. Usaha Bersama Maritim

- PT Muara Laju Lancar

- Other Prominent Players

Market Segmentation Overview

By Vessel Type

- Terminal tugs

- River tugs

- Seagoing (coastal) tugs

- Ocean-going tugs

- Emergency towing vessels (ETVs)

- Anchor-handling tugs (AHTs)

- Offshore Support Vessels

- Marine Support Vessels

- Cargo Carrier

- Barges

- Shoalbusters

By Power

- < 1000 HP

- 1000-2000 HP

- 2000-3000 HP

- 3000-5000 HP

- 5000-8000 HP

- 8000-12000 HP

- 12000 HP

By Application

- Harbor & Deep-Sea Carrier

- Product Carrier

- Gas Carrier

- Crude Carrier

- Petrochemical Carrier

- Others

- Salvage Operations

- Deep-Sea Towing

- Offshore Support

- Specialty Operations

- Others

By Ownership

- Third-Party Operators

- In-House Operators

By End User

- Shipping & Logistics

- Oil & Gas

- Defense & Navy

- Energy

- Construction & Infrastructure

By Country

- Malaysia

- Indonesia

- Myanmar

- Philippines

- Singapore

- Cambodia

- Thailand

- Vietnam

- Rest of South-East Asia

FREQUENTLY ASKED QUESTIONS

The South-East Asia tugboat charter services market was valued at US$ 1,046.50 million in 2024 and is projected to reach US$ 2,137.27 million by 2033, expanding at a CAGR of 8.40% during 2025–2033. Growth is driven by rising port throughput, offshore oil & gas activity, and the expansion of regional energy and infrastructure projects.

- Terminal tugs are the leading vessel category, accounting for over 21.08% market share, reflecting strong port activity across the region.

- By power, demand is highest for tugs in the 5000–8000 HP range, representing 22.45% of the market, as these vessels are essential for maneuvering mega-ships and supporting offshore energy operations.

The largest application is harbor and deep-sea carrier operations, which hold over 26.07% of market share. This includes support for container terminals, crude carriers, and LNG shipping. Offshore support services are also rising in importance due to oil, gas, and emerging offshore wind projects.

Third-party operators dominate with 54.76% market share, as shipping lines and port authorities increasingly outsource towage services for efficiency and cost savings. Leading companies include MCL Logistics, Lunar Shipping Malaysia, Swire Pacific, GAC, Haivan Ship, and Thoresen-Vinama, alongside regional players in Malaysia, Indonesia, and Singapore.

Singapore leads the market with more than 34% share, supported by its status as a global maritime hub and leader in digital and green shipping corridors. Malaysia follows with strong offshore energy projects and port expansions, while Indonesia and Vietnam drive demand through raw material transport, LNG infrastructure, and naval modernization programs.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |